The insurance industry has made tremendous progress digitizing claims. But in some cases, the drive to simplify claims has blurred the line between death notification and beneficiary verification. That distinction matters because allowing anyone to submit a beneficiary claim before verifying entitlement can create competing claims, unnecessary operational work, and poor customer experiences.

We used to support this model as well. Today, we recommend against it.

Here's why.

The moment someone completes a beneficiary claim form, an assumption has already been made: that the person submitting the claim is entitled to the proceeds.

The problem is that assumption is often wrong. Beneficiaries change all the time. People get married. People get divorced. Estate plans change. Children are added. Beneficiaries are removed. Relationships evolve.

Let's use a simple example. A granddaughter was once listed as a beneficiary on her grandmother's policy. Years later, the beneficiary designation was changed and she was removed. The grandmother passed away. The granddaughter finds the policy information and submits a claim online.

If your process allows anyone to submit a claim without validation, you've now created a problem that didn't need to exist. The claimant believes she's entitled to the proceeds. When your claims team eventually discovers she isn't, they now have to explain that she's not the beneficiary of record.

If you’ve ever been on the other end of that phone call, you know that's not a great experience for anyone involved. The result is higher call volume, longer handle times, and increased frustration for everyone involved.

Once an individual submits a claim, they naturally assume they have a right to the benefit. When you later tell them they're not the beneficiary, you're no longer dealing with a simple claim. You're dealing with a competing claim.

At that point, the organization isn't resolving a claim. It's resolving a dispute. A dispute that can lead to months, or even years of back-and-forth communication and litigation, all while interest fees compound.

In some situations, the issue can be resolved through documentation and communication. In others, you may need:

All because the process allowed someone to submit a claimant statement before confirming they had the right to do so. The irony is that these situations are often completely avoidable.

One of the most overlooked consequences of open claim form submission is the operational burden it creates. Every claim form submitted by someone who isn't the beneficiary creates work. Claims professionals must:

None of this activity helps pay the rightful beneficiary. It simply consumes resources that could be focused on processing legitimate claims and accelerating payments.

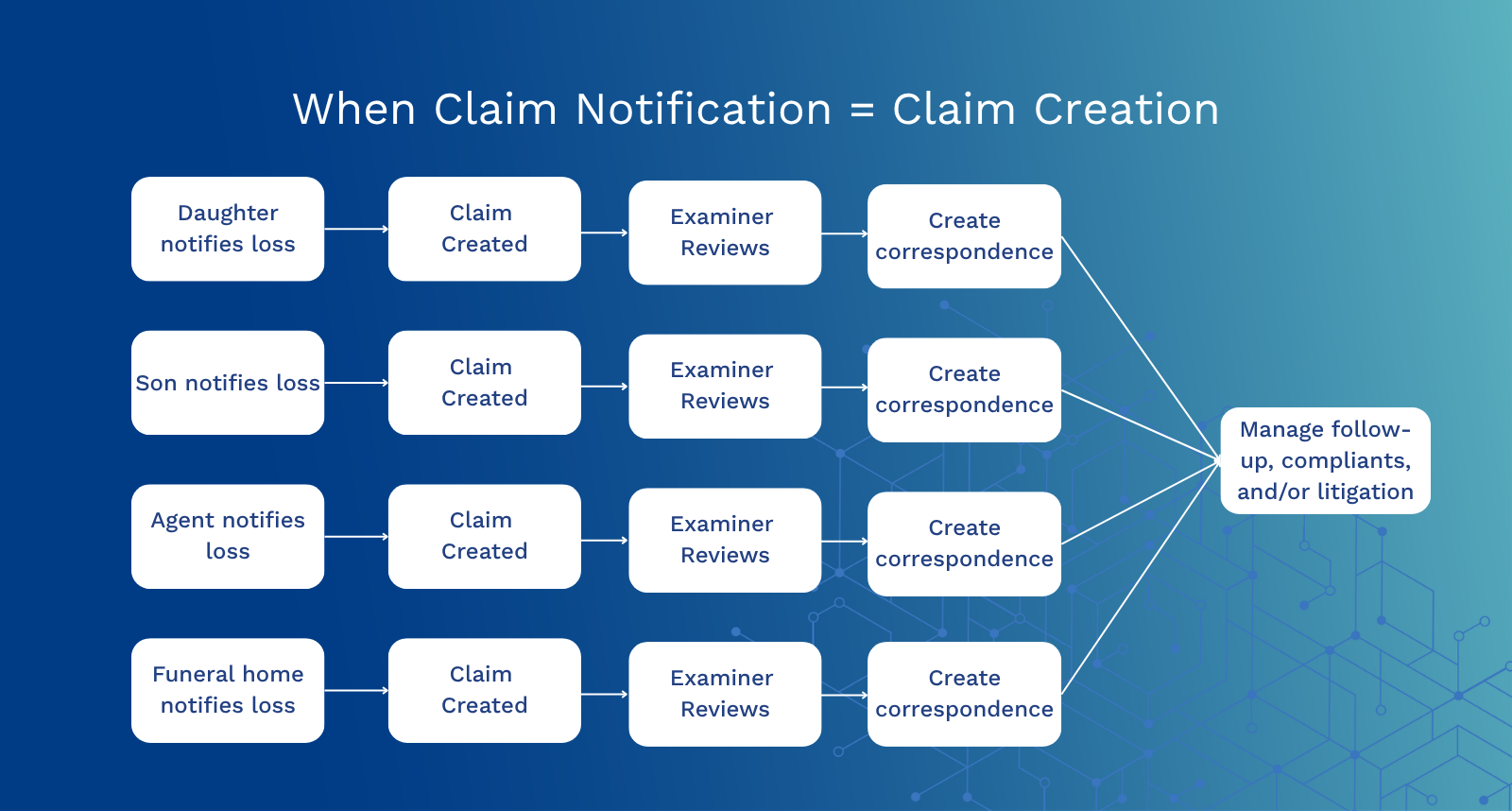

One of the most common arguments for open claim submission is that it makes it easier for people to notify the carrier that a death has occurred. The distinction comes down to two different questions. Death notification answers the question, "Has a death occurred?" Beneficiary verification answers the question, "Who is entitled to the proceeds?" Effective claims processes treat those as separate decisions.

But notification and claim submission are two completely different processes. A death notification can come from:

Not everyone who knows about a death is the beneficiary.

The solution isn't to allow everyone to file a beneficiary claim. The solution is to separate death notification from beneficiary claim initiation. Allow anyone with relevant information to notify you that a death has occurred. Then identify and engage the verified beneficiary. Those are two different workflows serving two different purposes.

This principle also applies to funeral homes and other third parties. They play an important role in notifying carriers and providing documentation, but notification should not be confused with beneficiary claim initiation.

Beyond the operational challenges, there are also privacy and fraud considerations. When organizations allow claim submissions without verifying beneficiary status, they risk exposing policy information and claim processes to individuals who may not have a legitimate interest in the contract.

While most submissions are made in good faith, strong verification practices help:

These protections benefit both the carrier and the beneficiary.

Sometimes the industry measures success by how easy it is to submit a claim.

That's the wrong metric.

If a process creates competing claims, generates unnecessary correspondence, increases call volume, frustrates customers, and diverts resources away from legitimate claimants, then it isn't simplifying the claims experience. It's creating avoidable complexity.

The best claim experiences balance convenience with verification. They allow anyone with relevant information to report a death while ensuring that beneficiary claims are initiated by the people who are actually entitled to receive the benefits.

Because at the end of the day, the objective isn't to collect claim submissions. The objective is to get the right payment into the right hands as quickly as possible.